I talked a lot about uncertainty in the last update, specifically around the subject of inflation and interest rates. In the UK we at least know that the long-awaited general election will be on the 4th of July. The prime minister had said that an election would happen in the second half of the year and so, much like his promise to grow the economy, he technically kept his word, if only just (GDP is up 0.2% over the last year). In a similar vein, he may have had about as much control over the timing as he did over recent falls in inflation (another of the five pledges he set out in January) with one MP saying that recent economic data were perhaps as good as they were going to get.

There is always speculation about why governments choose to hold an election at any given point. This time we’ve had suggestions that it might be about cashing in on excitement around the Euro 2024 football competition, or maybe that it’s connected to when school holidays start in Scotland. In reality, it’s more likely that the Conservatives are hoping that lower inflation will allow the Bank of England (BoE) to cut interest rates this month, helping to give the impression that conditions are improving.

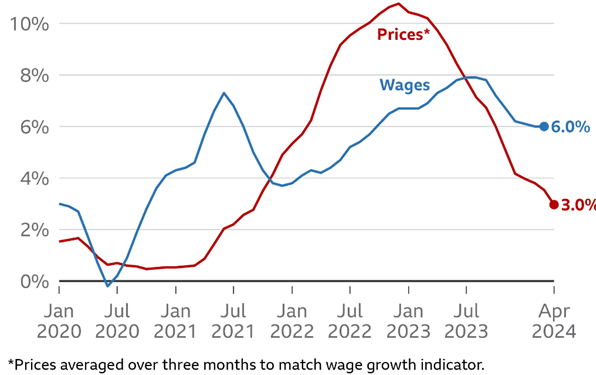

Mortgage rates in the UK had already started to fall in anticipation of future cuts, but recent inflation data were not quite as positive as had been predicted. The BoE had forecast that April’s inflation rate would be 2.1%, pretty much in line with their main target, however, the rate came in at 2.3%. Services inflation (another key metric which covers categories like hospitality and culture) was also worse than expected. This contributed to a fall in the chance of a June rate cut from 50/50 to more like 15%.

As mentioned in the last update, a reduction in the energy price cap by Ofgem, the energy regulator, was a big help in bringing the overall rate down. In total we’ve seen a greater than 27% fall in fuel prices over the last year, the largest fall on record. Of course, inflation is simply the rate at which prices increase and the slowdown this year doesn’t mean that the weekly shop is suddenly cheaper. The positive news is that average wage growth remains above inflation and if mortgage rates continue to come down then that will be a boost for retailers as consumers should have more money to spend.

Annual wage and price growth in the three months to April 2024

Source: ONS via BBC

While our improving picture is largely reflected in Europe, the same cannot be said for the United States where inflation remains some way above the level that the Federal Reserve (Fed) would like to see. The latest update for April showed that the rate was 3.4% which was in line with expectations and improves on previous month’s unexpected rise, but it suggests that the Fed are unlikely to be able to cut interest rates before America heads to the polls in November. In fact, the minutes from the last Fed meeting where rates were kept at a 23-year high range of 5.25-5.5%, indicated that some rate setters were open to raising rates further should inflation become more aggressive.

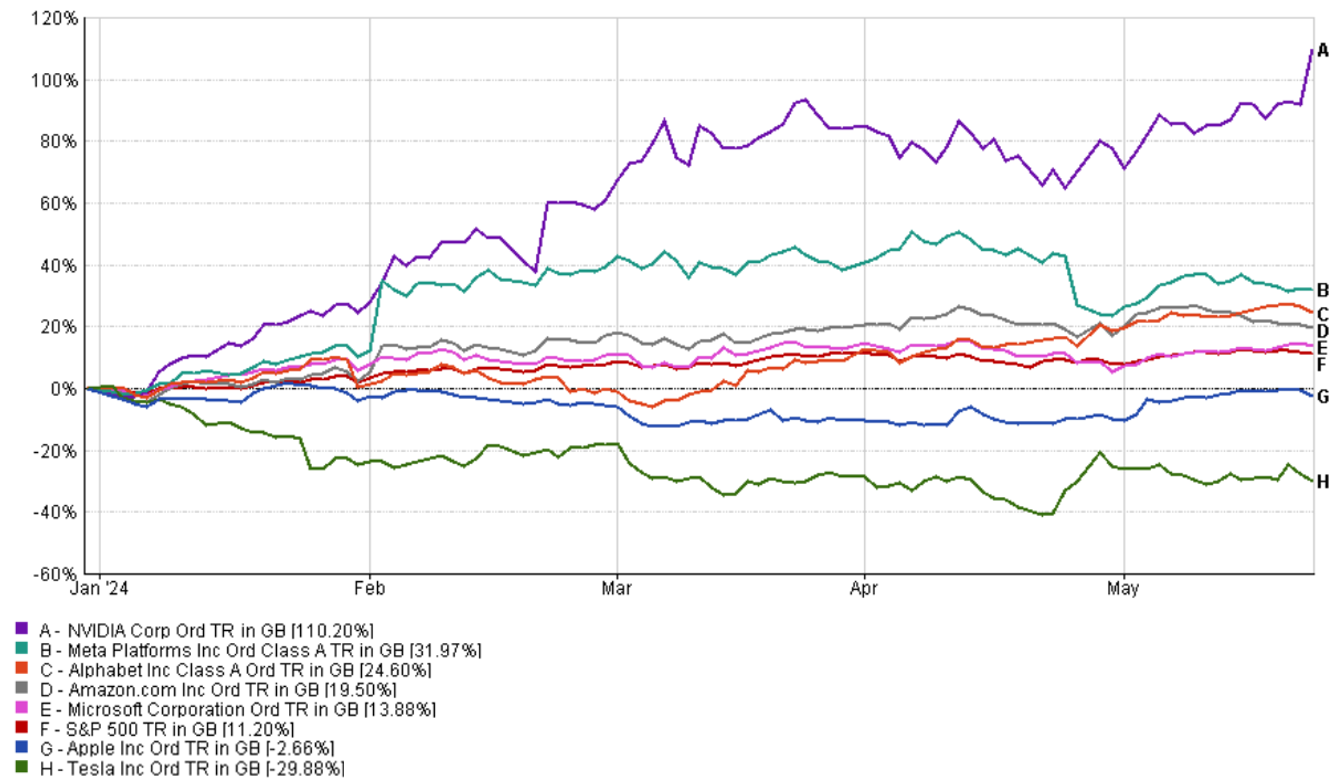

Somewhat surprisingly, the news was not enough to stop the main US markets hitting new all-time highs on the day. On that note, it’s worth taking some time to look at how the Magnificent Seven are doing following all the attention they garnered in previous updates. The group has essentially split into three. Shares in Nvidia, the computer chip maker, have more than doubled so far this year, capped by a 9% leap at the end of last month following the latest earnings data which showed that there is still a huge demand for its products. In fact, the shares are now so expensive that the company has announced a 10-for-1 stock split to make them more affordable.

The next group consists of Microsoft, Meta (the Facebook owner), Amazon and Alphabet (Google’s parent company). They’ve all enjoyed strong growth this year, but there is an expanding gulf between them and Nvidia as excitement over artificial intelligence shows no signs of abating. These “fab five” stocks (as they’re starting to be called) remain essential parts of many investment funds and still represent a significant portion of the global equity market.

This leaves us with Tesla and Apple which are lagging behind their peers in the face of challenging conditions and rising competition in their main markets. Apple remains the world’s second largest company based on the value of its shares, but it is largely flat so far this year and has missed out on the surge seen elsewhere. The phone maker is on the hook for huge pay-outs to its customers after it lost a court case about deliberately slowing down devices and it is also struggling to create a buzz for its latest offerings while losing market share to rival firms.

Last, and very definitely least, Tesla has experienced a similar problem to Apple, albeit over a more compressed timescale. Like Apple, which revolutionised the mobile phone market in 2007 when it launched the first iPhone, the unveiling of Tesla’s Model S in 2012 made electric cars exciting and it eventually rocketed the share price above $400 at the end of 2021. Things look very different now though with the company having to slash prices to try to compete with cheap alternatives coming out of China. Tesla's share price has more than halved since the peak and is down around 30% this year.

Magnificent Seven share price performance for the year to date

Source: Financial Express Analytics. To 24/05/2024 in pounds sterling

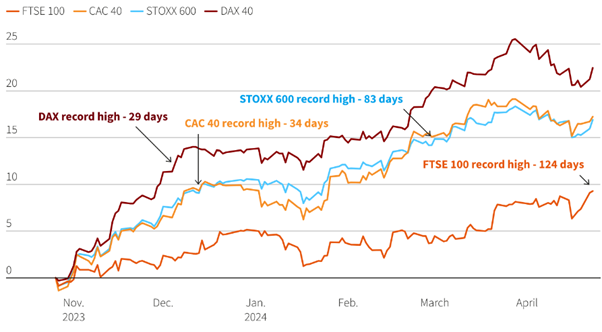

In many ways this presents a more interesting environment in which to invest as it means the skills of individual fund managers, as well as our own asset allocation decisions, can have more of an impact on performance. It also gave other markets, like those in Europe and the UK, a chance to shine with the FTSE 100 recently surpassing the record high it set just over a year ago.

Our headline index has benefitted from a weaker pound as many of the largest firms make their profits in dollars and receive a boost when these are converted to sterling. In addition, UK share prices remain very cheap, especially compared to those in the US, and investors have been taking advantage of this fact. Whilst the recovery should be celebrated, we took four times longer than Germany to recover from last October’s low point and we continue to lag behind much of Europe.

Europe’s recovery from October’s lows

Source: LSEG/Reuters

So, UK equities are doing ok, Europe is doing a bit better and the US is carrying on despite some challenges. Interest rates should also start to fall this year which will cause bond prices to rise, benefitting the fixed income portion of our portfolios. This is all good news but without wanting to end this update on a sour note, there are a couple of factors which we’ve got our eyes on because they could be headwinds over the rest of the year.

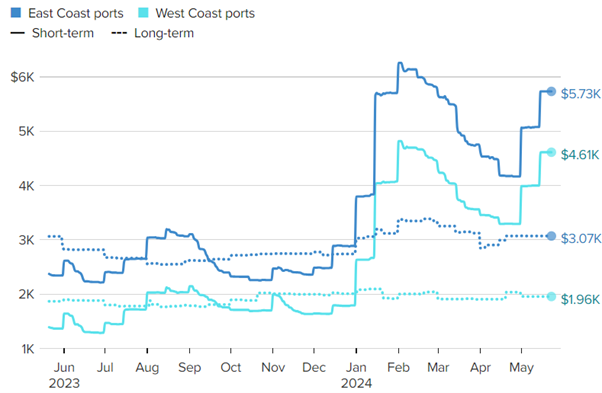

One of these is a recent spike in the cost of transporting goods by containership. We covered some of the issues in this sector earlier in the year including droughts that impacted on journeys via the Panama Canal and pirate attacks around the Red Sea that forced ships to take longer and more expensive journeys around the Cape of Good Hope.

As we head into the peak shipping season, these pirate attacks are on the rise which has coincided with bad weather in Asia. This has led some contracts to more than double in a month which is a concern because if these higher costs are passed onto consumers and inflation rises, it would be bad news for interest rates.

Daily average shipping prices for goods coming into the US from East Asia.

Source: Xeneta as at 23/05/2024

A more troubling concern are the escalating tensions between China and Taiwan which have worsened following the election of a new Taiwanese president. The Chinese see his comments about Taiwan's independence as a challenge to their “one country, two systems” approach to areas they perceive to be under their governance. Recent naval exercises around the island are a rehearsal for a potential invasion and the accompanying rhetoric is growing increasingly threatening.

Obviously, the potential for another regional conflict while Ukraine is still under attack from Russia and Israel continues its attempts to wipe out Hamas would be very concerning from a humanitarian perspective, but China’s importance to global trade would mean that any military action would also be a major test for markets. I should emphasise that few experts are predicting that China will go beyond intimidation tactics and we haven’t adjusted our strategy as a result of these events, but I think it’s important to highlight issues which have the potential to disrupt global supply chains and cause volatility to increase.

Market and sector summary to the end of May 2024

Source: Financial Express Analytics.

Past performance is not a guide to future performance, nor a reliable indicator of future results or performance.