Thank you to everyone who has already responded to the latest review of the IMS portfolios which was sent out last month. We’ve had an excellent response so far, but if you have not yet had an opportunity to send us your acceptance, we would be grateful if you could so that we can make sure your investments are in the latest fund selection. You can respond to this message if you would like another copy of the review to be sent out.

Our latest quarterly review covered the period up to the end of October and therefore did not discuss the outcome of the US election. With the results now in, markets have shifted their focus to the potential economic and policy implications of Donald Trump’s second term as US president.

In addition to beginning to assign people to key positions, his administration has already outlined plans aimed at stimulating domestic economic growth through a combination of tax cuts, deregulation, and a renewed emphasis on reshoring manufacturing. These policies have been met with optimism in sectors like energy and industrials, where regulatory easing and infrastructure spending could provide tailwinds.

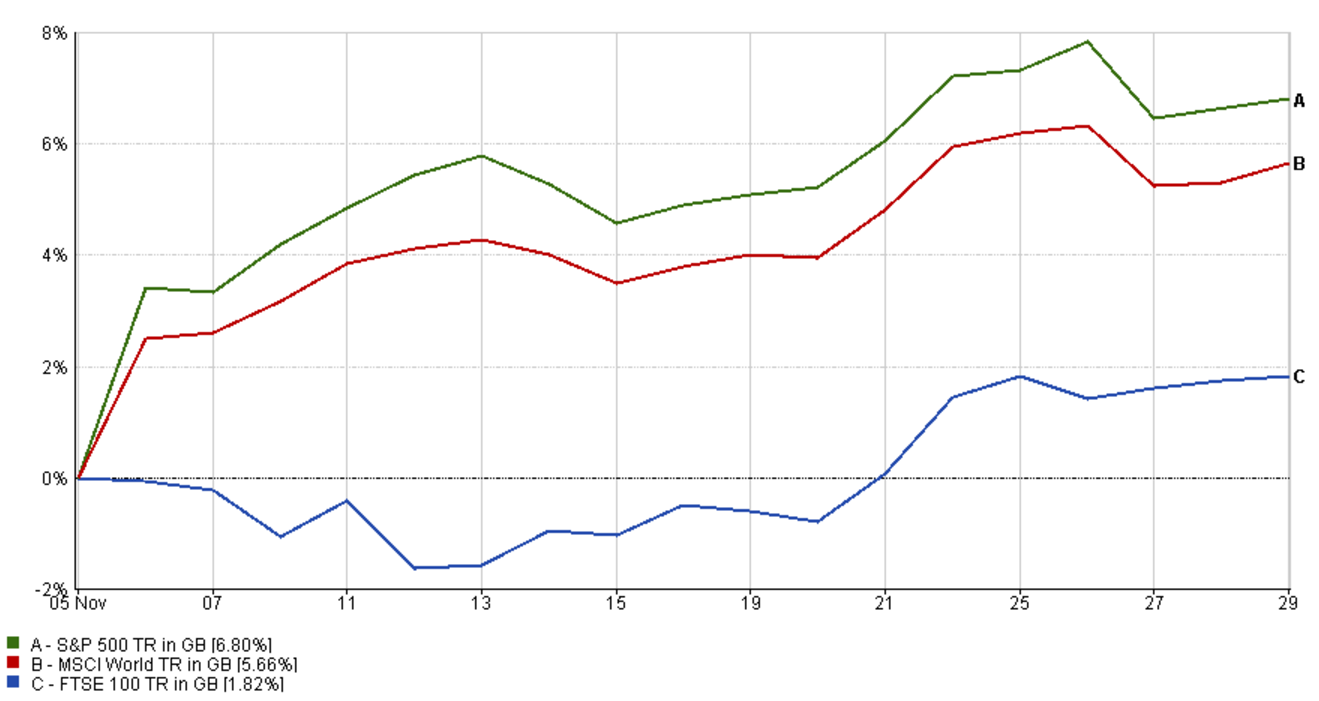

Post-election market rally

Source: Financial Express Analytics, 5/11/24 – 29/11/24

However, concerns remain regarding the potential for heightened trade tensions, particularly with China, the European Union, and other key trading partners. The Trump administration has already signalled its intention to reintroduce tariffs on a range of imported goods, including technology components, consumer electronics, and automotive parts. The proposed tariffs could range from 10% to 25%, with China being a primary target, alongside possible levies on European car exports and certain agricultural products from Latin America.

If implemented, these tariffs could have several ripple effects on global markets. Higher import costs may lead to increased prices for US consumers, potentially dampening domestic demand and eroding corporate profit margins in industries reliant on international supply chains. Sectors such as technology, automotive, and consumer goods could face higher costs, which may force companies to either absorb the impact on their profits or pass it on to consumers, contributing to inflationary pressures. These pressures could be exacerbated by efforts to reduce immigration or to expel existing migrants which would increase the cost of services as the labour pool falls.

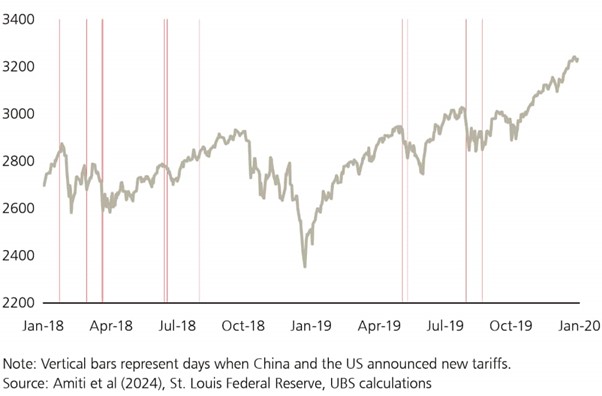

Market reactions to previous tariff events (red lines indicate US or retaliatory Chinese tariffs)

Source: UBS, S&P 500 index

In addition, tariffs on European goods could exacerbate existing tensions between the US and the EU, leading to retaliatory measures that may disrupt transatlantic trade flows. The automotive industry, which is heavily integrated across both regions, is particularly vulnerable. A 20% tariff on European car imports, for example, could significantly reduce demand for German and French exports, potentially impacting growth in already sluggish European economies.

Meanwhile, tariffs targeting China would likely reignite trade disputes that unsettled markets during Trump’s first term. While the initial round of tariffs had a noticeable impact on Chinese exports and manufacturing, China has since sought to diversify its trading partners and strengthen regional ties. However, further tariffs could still weigh heavily on China’s economic recovery, particularly as it continues to grapple with weak consumer demand and a fragile property sector.

China has recently implemented a series of stimulus measures to revitalise its slowing economy. The People's Bank of China has reduced interest rates and eased reserve requirements for banks to encourage lending and investment. Additionally, the government has pledged to increase fiscal spending, particularly on infrastructure projects. These measures aim to stimulate economic growth, boost consumer confidence, and stabilise the struggling real estate sector. However, it is widely believed that further action may be taken once there is greater clarity on Trump's trade polices.

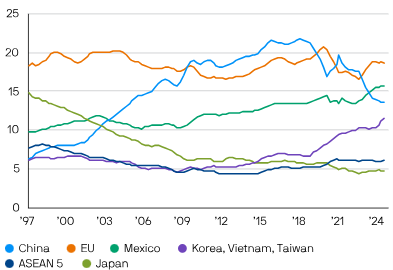

Chinese imports into the US have remained low since Trump's first term

Source: LSEG Datastream, US Census Bureau, J.P. Morgan Asset Management. Percentage of total goods and services imports, 4-quarter moving average. Data as of 12 November 2024.

For much of the year, markets have been confident that inflation was going to fall and that central banks would cut rates in response but the outlook now appears less certain. While inflation has moderated in some regions, recent data releases show that it has risen again in the US, EU and UK. Central banks, including the US Federal Reserve and the European Central Bank, have reiterated that any move to lower interest rates will be contingent on sustained progress toward their inflation targets. The Bank of England faces a similar challenge, with inflation still running above its 2% target, despite early signs of a slowdown in consumer spending and wage growth.

One impact of this shifting outlook is that bond yields have been rising recently. This might seem counterintuitive as yields tend to fall when interest rates fall and all three of the banks above have implemented a number of cuts this year. However, central banks primarily impact short term borrowing costs while longer term rates tend to be influenced by what investors think will happen to inflation in the future. 30-year Gilt rates recently passed 5% which is the highest level for over 20 years. This seems excessive and we are not alone in thinking that the market has moved too far, too quickly.

The broader concern for investors is that escalating trade tensions could lead to a more protectionist global environment, reducing overall trade volumes and slowing global economic growth. While certain domestic industries may benefit from protectionist policies in the short term, the long-term impact on global supply chains and cross-border investment could be more negative. As such, markets have started to price in higher levels of volatility, reflecting uncertainty around how these trade policies will unfold and their potential economic consequences.

Of course, we also have to be aware that the threat of tariffs is sometimes used as a negotiating tactic and it would be unwise to make any definitive assumptions at this stage. Central banks must attempt to balance the potential boost to demand from tax cuts against the potential drag from migration and trade tensions. It is important to remain focused on the long term benefits of our diversified and balanced approach, especially following such a sustained rally in US markets.

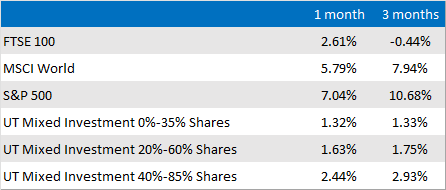

Market and sector summary to the end of November 2024

Source: Financial Express Analytics.

Past performance is not a guide to future performance, nor a reliable indicator of future results or performance.