Firstly, on behalf of the IMS team, I’d like to wish you a happy and healthy new year. I hope you had an enjoyable break (if you were able to have one).

While 2024 was heralded as a year when nearly half the global population went to the polls, geopolitics ultimately stole the spotlight from electoral outcomes. Significant political events in France, Syria, and Eastern Europe created ripples of uncertainty, but they had surprisingly little impact on market sentiment. Instead, investors’ attention was dominated by broader themes, including trade disputes, energy market dynamics, and central bank policies, which are now shaping the investment landscape as we head into 2025.

The previous monthly update made reference to how markets were beginning to react to Donald Trump’s recent re-election and we’ve seen further evidence of this of late. OPEC (Organization of the Petroleum Exporting Countries) announced a significant cut in output for 2025 in an effort to stabilise prices. Having nearly hit $90 a barrel in April, the price has been volatile since and fell back below $70 at one stage. This decision reflects concerns about weaker global demand and potential disruptions from US trade tariffs. OPEC’s latest intervention, combined with shifting consumer patterns and renewable energy trends, suggest that oil markets could face a volatile year ahead.

In the US, inflation rose to 2.7% in November, complicating the Federal Reserve’s plans for 2025. While many expected a pivot to interest rate cuts, core inflation in areas like housing and services continues to exert pressure, leading to rising bond yields and a cautious approach from investors. US equities have remained a cornerstone of global markets, buoyed by the enduring strength of the US economy even amid a backdrop of geopolitical tensions and inflationary pressures. Consumer spending, which has been a vital engine of growth, continues to defy expectations, supported by a resilient labour market. Corporate earnings have also demonstrated robustness across key sectors, with tech and industrials leading the charge despite headwinds from higher interest rates.

US household exposure to equities is at a record high

Source: Schroders

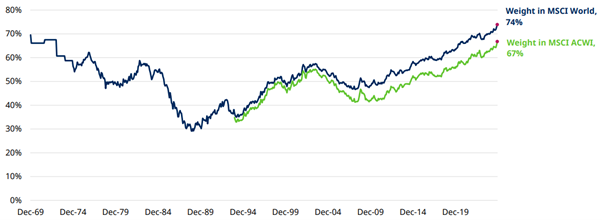

The global reach of US-listed companies has further cemented their appeal, with US equity markets delivering returns more than double that of most other major regions last year. This strength has not gone unnoticed by investors, with global portfolios maintaining significant exposure to US markets. However, with valuations remaining elevated and inflation still above target, the sustainability of this performance will be closely watched as we move through 2025.

Proportion of US equities in global markets

Source: Schroders

Elsewhere, China has been stepping up its activity ahead of Trump’s inauguration. Alongside a ban on rare earth mineral exports (vital for the production of all things high-tech) to the US, they have also launched a probe into NVIDIA. The investigation is based on reported concerns about the chipmaker’s dominance of the market and breaches of agreements related to past acquisitions. Both announcements came after the US revealed details of export controls on NVIDIA’s premium products which are intended to hamper China’s development of advanced AI. Nvidia’s share price finished December 2.33% lower having fallen as much as 8% at one point during the month.

The Chinese update also outlined its efforts to stimulate its economy. President Xi recently insisted that the country would remain the engine of global growth in 2025 and the Chinese government announced this week that it would be moving its monetary policy from 'prudent' to 'moderately loose'. Whilst a pretty dry statement at face value, this is the first change in 14 years and it helped to lift local markets. We expect to see further news on this front over the coming months and, in conjunction with US trade tensions, it gives us a flavour of the sort of investment environment which could be the key theme of 2025.

Closer to home we saw inflows into UK equities in November for the first time since May 2021. The £317m inflow is a drop in the ocean compared to the £25bn that's flowed out over the last 41 months, but it is hopefully the start of a positive trend. Part of this was a response to Labour’s first budget being less severe than expected in areas such as CGT and dividend taxation, but it’s also a reflection of the value offered by British firms following a long bull market for US stocks. This was highlighted by the more than £5bn worth of takeover bids that came in at the end of November.

With focus intensifying on America’s market dominance and concerns about debt levels (already suspected to exceed 100% of GDP) alongside political wrangling in the EU, might we be about to see the oft-touted re-emergence of UK stocks? Possibly, but as we enter 2025 the prevailing consensus is that the US will continue to dominate global markets, bolstered by its resilient economy and corporate strength.

However, this confidence comes with potential risks, particularly in light of President Trump’s proposed tariff plans. The reintroduction of significant taxes on imports from key trading partners like China, Mexico, and Canada could disrupt global supply chains and raise costs for US businesses and consumers. While certain domestic industries may benefit in the short term, these measures risk stoking inflation and dampening international trade, creating potential headwinds for US equities.

Such policy-driven uncertainties serve as a reminder of the dangers of groupthink. An over-reliance on US equities, despite their historical resilience, could leave portfolios vulnerable to shocks. As always, diversification across regions and sectors remains crucial to navigating an environment where geopolitical and economic surprises are likely to define the year ahead.

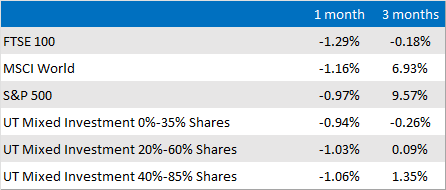

Market and sector summary to the end of December 2024

Source: Financial Express Analytics.

Past performance is not a guide to future performance, nor a reliable indicator of future results or performance.