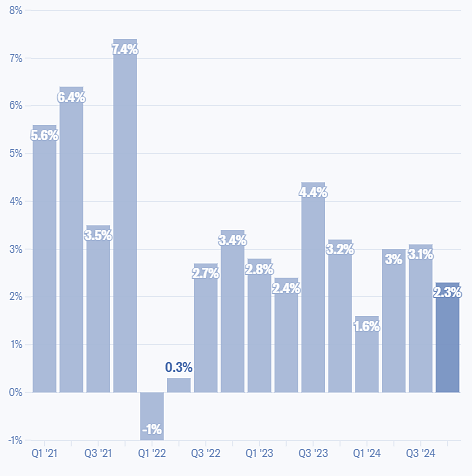

February saw global markets grappling with a shifting economic landscape as investors reacted to fresh data on inflation and economic growth, alongside worries about the impact of tariff policies. In the United States, concerns about the sustainability of recent economic strength started to emerge, with the latest GDP figures showing the economy grew at an annualised rate of 2.3% in the fourth quarter. While this met expectations, there were signs of slowing momentum, particularly in consumer spending and business investment.

US quarterly GDP growth

Source: Bureau of Economic Analysis

Equities reflected this caution, with major US indices struggling for direction. A significant factor in this downturn was the underperformance of the so-called "Magnificent Seven"—Apple, Microsoft, Amazon, Alphabet (Google's parent company), Meta Platforms, Nvidia, and Tesla. These technology giants, which had substantially contributed to market gains in previous years, faced headwinds in 2025.

The technology sector, which had been a key driver of gains in recent months, saw notable weakness as high valuations came under scrutiny and corporate earnings guidance hinted at a more uncertain outlook. For instance, Microsoft experienced a decline of nearly 6% year-to-date, reflecting investor scepticism over the potential returns on heavy capital spending amid rising AI competition.

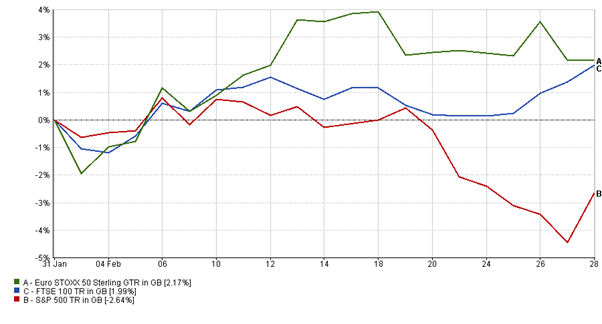

The S&P 500 fell approximately 1.5% in US dollar terms over the month. However, due to the pound strengthening against the dollar, the index saw a steeper decline of around 2.64% when measured in sterling, highlighting the impact of currency movements on returns for UK-based investors. This collective underperformance raised questions about the sustainability of their growth trajectories and their impact on the broader market.

The Federal Reserve (Fed) opted to leave interest rates unchanged, in line with market expectations. Despite Donald Trump’s vocal calls for lower rates, minutes from the Fed’s latest meeting suggest policymakers are in no rush, preferring to wait for “further progress on inflation.” Adding to their caution, the bank is wary of Trump’s proposed tariffs, which could push prices higher. As a result, markets are now assigning a greater probability to zero rate cuts in 2025.

In the UK, where GDP was unexpectedly 0.1% higher in the final quarter of 2024, the Bank of England took the market by surprise, not by cutting rates (this was widely expected) but by the level of support for the cut by the bank’s rate setters. Every member voted for a cut with the 0.25% reduction taking the headline rate to a 20-month low of 4.5%. However, two members opted for a full half point cut, including one who until the latest vote had been against making any reductions at all.

Although recent GDP moves give some hope, the UK’s economic landscape remains more fragile than in the US. Inflation remains a challenge, though there are signs that pressures are beginning to ease, particularly in energy and food prices. Despite these headwinds, the FTSE 100 gained 1.99% in February, benefiting from stronger performances in defensive sectors and a weaker pound boosting multinational earnings.

Market performance divergence

Source: Financial Express Analytics, 01/02/2025-28/02/2025

The contrast between the US and other major economies has become more pronounced. While the US has remained relatively strong, the latest data suggests this outperformance may not be as robust as previously thought. Trade tensions, fiscal policy uncertainty, and slowing consumer demand all add to the risks facing the world’s largest economy. Meanwhile, the UK and Europe are contending with their own set of challenges, but policymakers appear increasingly focused on supporting growth rather than solely prioritising inflation control.

Adding to global uncertainty, the month ended with a astonishing diplomatic fallout between Ukrainian President Volodymyr Zelensky and the US President. Tensions flared following Trump’s remarks on US military commitments in Europe, raising concerns about Washington’s future stance on the Ukraine conflict. Market sentiment reacted to the potential geopolitical consequences, with defence stocks in Europe seeing renewed interest amid speculation of increased military spending. The development has also cast doubt on the prospects for a negotiated peace settlement in Ukraine, reinforcing the shift in market momentum towards greater caution on US foreign policy and its broader economic implications.

Looking ahead, we will be watching key data releases, including inflation updates and employment figures, for further clues about the direction of monetary policy. Market volatility is likely to persist as confidence in economic growth fluctuates. While optimism remains in some areas, there are clear signs that momentum is shifting, particularly in the US, where expectations for sustained strength are now being reassessed. Portfolio positioning will remain critical in navigating this evolving environment, with diversification and careful risk management playing an essential role in balancing opportunity and uncertainty.

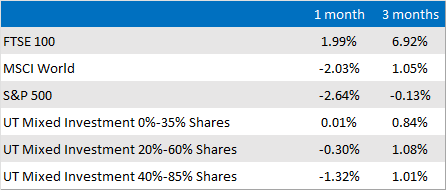

Market and sector summary to the end of February 2025

Source: Financial Express Analytics.

Past performance is not a guide to future performance, nor a reliable indicator of future results or performance.