The dominant market theme in March remained consistent with previous months - US equities continued to experience high volatility, largely driven by structural weaknesses in the American economy and Donald Trump’s increasingly aggressive stance on international trade.

The sharp and concentrated selloff in US large-cap technology stocks - particularly the Magnificent Seven - has been the key story. These stocks, the main drivers of the rally over the last couple of years, have collectively lost hundreds of billions in value in recent weeks, dragging down broader indices.

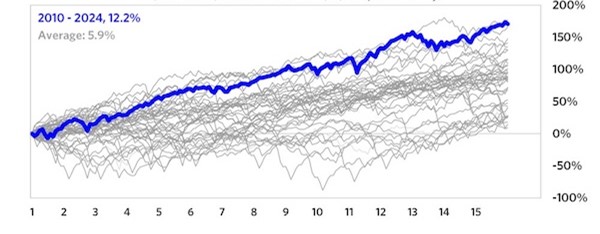

In many ways, this isn’t all that surprising. Trump’s election win led to a surge in US stocks as investors priced in a lower tax, lower regulation environment and a subsequent rise in corporate profits. This compounded the long run of success for US companies which has seen the last decade and a half become the best 15-year period since 1970, with returns double the average level.

US equity performance over every 15-year period since 1970

Source: Bridgewater via investing.com

As such, it is not a shock that fears about the economic outlook have seen the most valuable stocks tumble. The impact has been exacerbated by a fall in the US dollar which means that the c4.5% S&P 500 decline in dollar terms has turned into a more than 7% drop from a UK investor’s perspective.

Tesla has been the worst performing member of the Magnificent Seven so far this year, reflecting concerns over weakening demand and rising costs. Somewhat ironically given Elon Musk’s close relationship with the US president, the firm has raised concerns about US trade policy, writing to the government to warn that recent penalties on Chinese imports are hurting its cost base while retaliatory tariffs on EV imports are hitting its sales. The company has urged policymakers to reconsider the scope of these policies, highlighting the broader impact on supply chains and pricing pressures across the sector. These concerns extend beyond technology stocks, with US companies in manufacturing, consumer goods, and autos raising alarm over rising input costs.

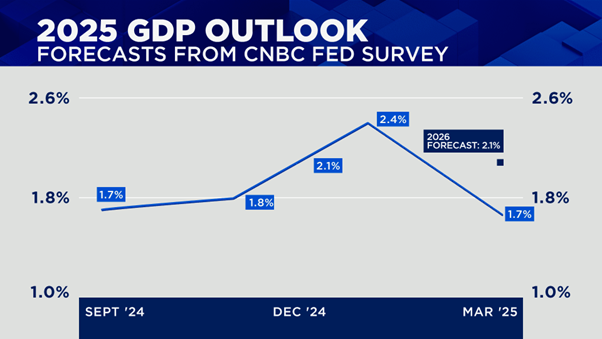

As expected, the US Federal Reserve chose to keep interest rates unchanged at its latest meeting, but the accompanying commentary was more revealing. In line with other forecasters, they have cut their expectations for US GDP growth from 2.1% to 1.7% while increasing inflation estimates. Tariffs were highlighted as complicating the process of bringing inflation under control.

US GDP expectations

Source: CNBC Fed Survey

Conversely, inflation in Europe registered another fall last month and now stands at 2.3%. This increases the likelihood that the European Central Bank will implement a further interest rate cut when they meet later this month, after recently lowering the rate to 2.5%. Meanwhile, in Germany, the announcement of a significant stimulus package from the incoming chancellor has drawn a lot of attention. The package, now approved by parliament, removes defence spending from debt calculations and includes plans to spend €500bn on infrastructure improvements. The proposals are widely seen as a response to American trade aggression.

Investors have taken note of weakening US GDP forecasts, with analysts increasingly citing trade policy as a headwind to growth. While economic data, particularly employment figures, have remained firm, the risk of policy-driven inflation and its potential to limit future rate cuts is unsettling markets. Goldman Sachs recently slashed its growth expectations for the US from 2.4% to 1.7% and JPMorgan is now factoring in a 40% chance of a US recession. These are both very large shifts from the start of the year.

Many investors had expected that President Trump, known for his close attention to stock market performance, would step in to reassure markets if equities suffered significant declines. However, recent statements suggest a shift in his focus. In a Fox Business interview, Trump dismissed business concerns over his trade policies, stating that such measures are necessary for the long-term strength of the US economy.

Treasury Secretary Scott Bessent reinforced this stance by downplaying recent market weakness, emphasising that the administration is focused on long-term economic fundamentals rather than short-term volatility. His remarks that the White House is prioritising “Main Street over Wall Street” have unsettled investors, many of whom had previously relied on government support during market downturns.

At the end of the month, Trump announced a new 25% tariff on the import of foreign-made cars into the US, immediately leading to falls in the share prices of the main manufacturers (both American and non-American). The announcement is expected to be the opening salvo in a raft of new trade policies, dubbed “Liberation Day”. Trump has repeatedly altered his policies since he took office (often immediately after meeting the heads of impacted industries) and any future changes have the potential to send markets in a different direction, but at some point (which might have already passed), the damage is already done.

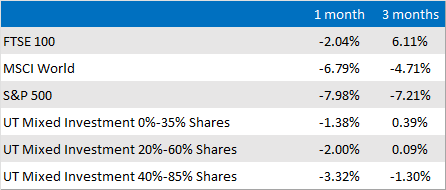

The important thing to highlight is that despite the severity of the declines in large-cap technology companies, this is not a broad market selloff. European markets have proven far more resilient by comparison, with key indices such as the Euro Stoxx 50 and FTSE 100 holding up much better.

European outperformance

Source: Financial Express Analytics, YTD 2025

The recent US-led selloff has largely targeted the largest and most overvalued companies, with investors rotating away from stocks that had seen excessive gains over the past year which is something that I’ve highlighted as a potential outcome for many months. The most expensive companies have been priced for perfection and (as we saw with the damage to Nvidia’s share price when the Chinese AI Deepseek launched) any challenge to momentum has led to immediate volatility.

This shift has favoured value-oriented and more reasonably priced companies, which make up a larger share of European indices. Unlike the US, where the market has been concentrated in a handful of mega-cap names, Europe’s broader sector diversification and more attractively priced shares have provided a degree of insulation.

Whilst we would never be so bold as to suggest this is a permanent shift, the market recalibration away from overextended positions suggests a healthier backdrop for stock selection moving forward which should be of benefit to our style of investing.

Market and sector summary to the end of March 2025

Source: Financial Express Analytics.

Past performance is not a guide to future performance, nor a reliable indicator of future results or performance.